Scrabble-Weighted Portfolios

Why using scrabble tiles to pick stocks outperforms the SP500

In a world with crypto-trading hamsters, stock-trading cats, and all manner of arbitrary stock-selecting mechanisms, perhaps it's not so surprising that someone has looked at the use of board games to inform portfolio decisions.

At least that's one takeaway from a presentation by Cass Business School's Nick Motson, who found that a "Scrabbled-weighted portfolio" — one in which stocks are held in proportion to their tickers' corresponding tile values — outperforms the market over a long horizon. The presentation yields eye-popping figures showing 1.5% higher returns to the Scrabble Index over the market-cap weighted benchmark:

Of course, the larger point of his presentation is not that investors should go long the Scrabble Index, but rather thatOf course, the larger point of his presentation is not that investors should go long the Scrabble Index, but rather that in the space of possible portfolio weights, there are bound to be portfolios that ex post dominate the market portfolio (the implication being that one should be skeptical of "smart beta" strategies that purport to deliver higher sharpe ratios).

Scrabble Tile Value Distribution. Under the Scrabble Index, the ticker AAPL would have a value of 1.5 (calculated as (1 + 1 + 3 + 1)/4), while Tesla (TSLA) would have a value of 1 ((1 + 1 + 1 + 1)/4). Apple is thus held 3:2 in proportion to Tesla.

As a former competitive scrabble player turned finance PhD student, I couldn't help but dig deeper into the implications of a Scrabble-weighted portfolio. As a first pass, it is worth replicating the figure from Motson's presentation to check that the overall methodology is correct. Although I obtain slightly different numbers, the Scrabble Index does indeed **outperform the market-cap weighted index from 1969-2014, with annualized returns of 12.1% vs 10.3% for the value-weighted portfolio.

Scrabble-Weighted Portfolio. Portfolios use 500 largest stocks at each month-end with at least 5 years of continuous trading history.

It also achieves a higher Sharpe ratio of 0.132 vs. 0.114.

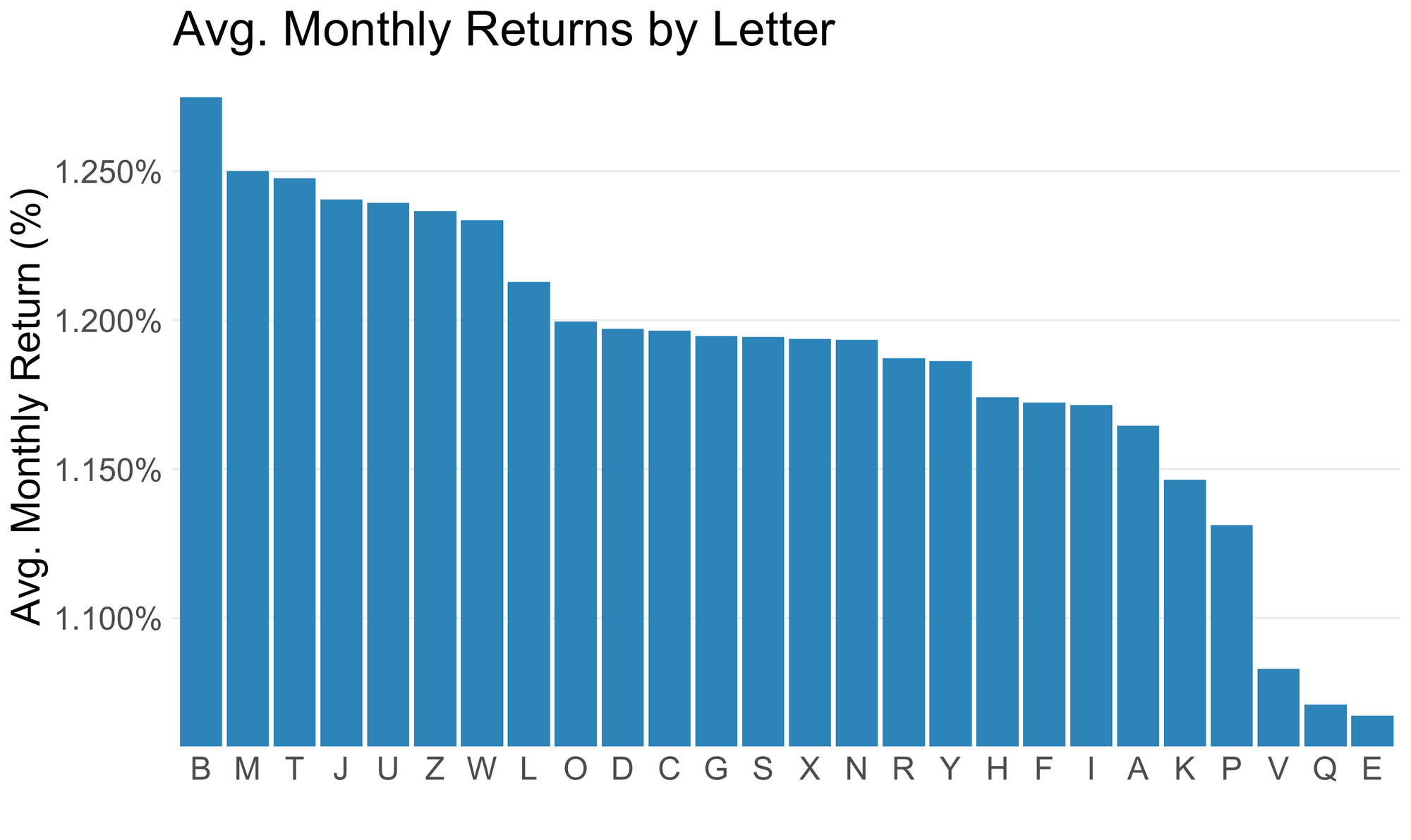

One answer for what's going on might be that the letters truly do have some meaning. Perhaps, for example, tech or growth companies are more likely to have X, Q, J, and Z in their tickers (think Xerox, Amazon, Zoom, etc.). Or, given the "size factor", where small stocks have historically outperformed large ones, it could be that tile value is correlated with its ticker's market cap.

None of this is really true. The correlation between ticker value and market cap rank is a mere 6%. The average returns by letter show some heterogeneity, but not one that reveals a clear split by tile value. (The error bars, not shown, are monstrous).

In tile value - return space, the lack of correlation is even more stark:

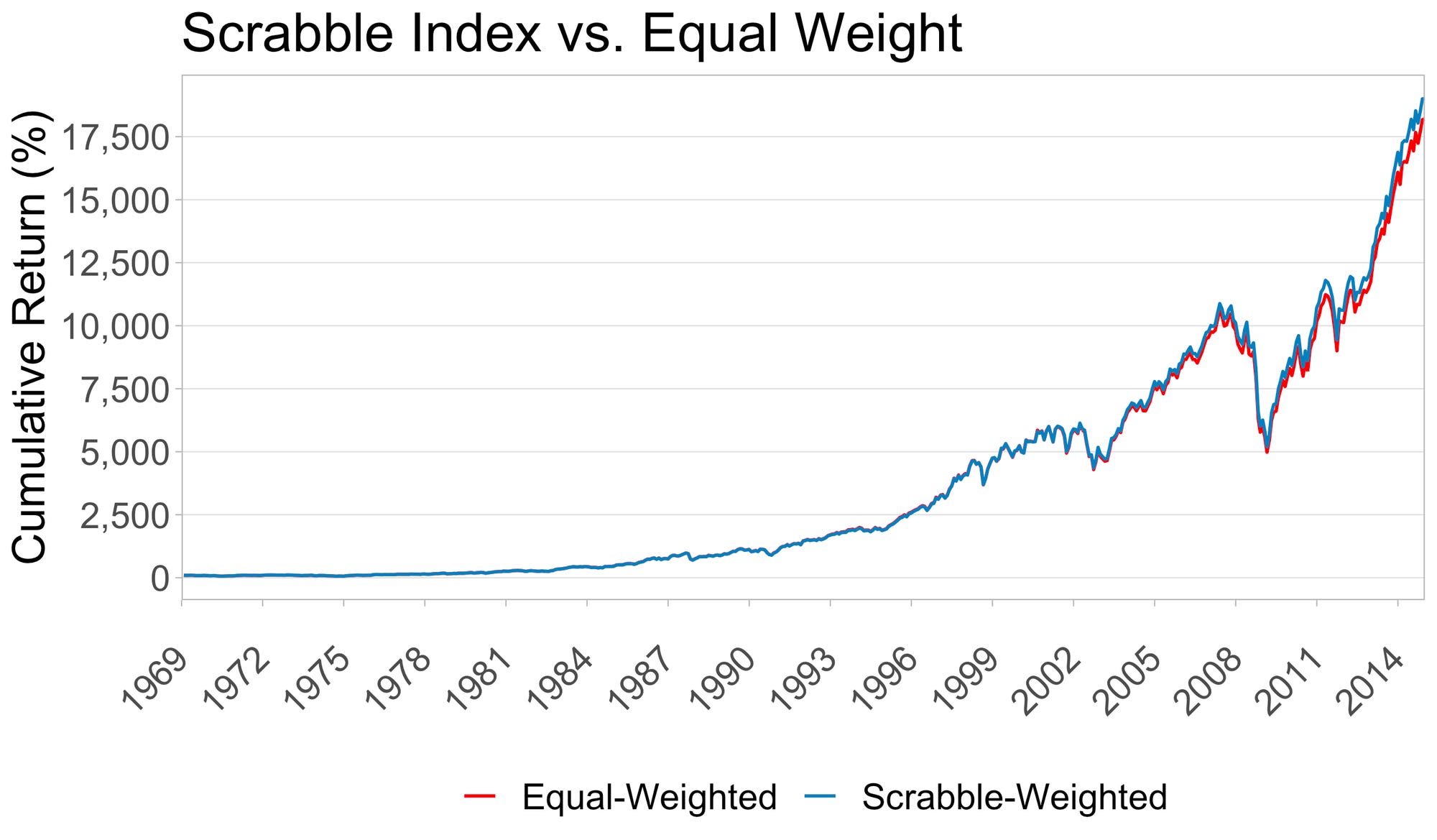

What's likely going on is exactly the opposite: if tile values have zero correlation with stock-related fundamentals, then weighting by tile value is similar to attaching roughly equal weight to each stock. In that case, the returns on the Scrabble portfolio would mirror the returns on the equal-weighted portfolio, which is basically what we see:

I think the broader lesson here is that the appropriate benchmark for a given set of prospective portfolio weights is not value-weighted indices like the S&P500. The null hypothesis — the hypothesis that obtains when weights are "meaningless" — is that stocks are sampled in equal proportion. Creating a portfolio weighted by the frequency of letters in one's own name would also likely outperform the value-cap index, but we would agree this isn't particularly meaningful. Given the widespread use of value-weighted indices as fund benchmarks, this point is more profound than it may seem. Is there a good reason we evaluate managers against an index that performs reliably worse than one selected on random (equal) weights?

In a world where I figure out how to make my code run faster, it would be interesting to see if there is a combination of tile values that delivers reliably higher risk-adjusted returns. I'm skeptical there is one (in-sample, let alone out-of-sample), but it's not impossible. After all, there is a large literature identifying ticker characteristics that seem to matter: ease of pronunciation, likeability, meaning, and linguistic similarity to other companies' tickers. (Other things, like ticker length, do not appear to matter.)

In the meantime, let's hope Dave Portnoy isn't worse off for using Scrabble tiles to select his stocks:

https://twitter.com/TheStalwart/status/1274066978911764488?s=20